Top Retail Companies by Revenue: 2026 Snapshot Based on Latest Available Data

Global Retail Revenue Leaders in the Latest Deloitte Edition

This ranking uses Deloitte Global Powers of Retailing 2025. The underlying company data are FY2023 retail revenues, defined as financial years ending between 1 July 2023 and 30 June 2024. The 2026 framing reflects the publication cycle of this page, not current-year sales.

Revenue is shown in US dollars, millions. The ranking compares retail scale, not total corporate size or profitability. For diversified groups, non-retail activities can be excluded or treated separately under the source methodology, which is why retail-revenue rankings can differ from consolidated corporate-revenue lists.

Key figures for the ranking

Overview: scale, format and geography

The largest retail companies are not only supermarket chains. The top group combines mass merchants, e-commerce platforms, warehouse clubs, pharmacies, home-improvement chains, discounters and food retailers. Walmart is the clear revenue leader, while Amazon and Costco form the next scale tier.

Continue exploring

More StatRanker rankings on public finance, tax burden, debt and government spending.

The upper part of the list shows three structural advantages: large domestic markets, recurring grocery and pharmacy spending, and logistics systems that can support either dense store networks or high-volume e-commerce. European discounters and food groups rank strongly because grocery demand is frequent, local and less cyclical than discretionary retail.

Top 10 retail companies by revenue

The Top 10 is dominated by US companies, but Germany and China are also present through Schwarz Group, Aldi and JD.com. The mix is important: the leaders include a warehouse club, pharmacy groups, a home-improvement chain, supermarket operators, discounters and a major e-commerce platform.

| Rank | Company | Country | Retail revenue |

|---|---|---|---|

| 1 | Walmart | United States | $648,125M |

| 2 | Amazon | United States | $251,902M |

| 3 | Costco | United States | $242,290M |

| 4 | Schwarz Group | Germany | $177,009M |

| 5 | The Home Depot | United States | $152,669M |

| 6 | The Kroger Company | United States | $148,905M |

| 7 | Aldi | Germany | $123,608M |

| 8 | JD.com | China | $122,884M |

| 9 | Walgreens Boots Alliance | United States | $121,191M |

| 10 | CVS Health | United States | $116,763M |

Retail revenue in US$ millions. Source edition: Deloitte Global Powers of Retailing 2025, FY2023.

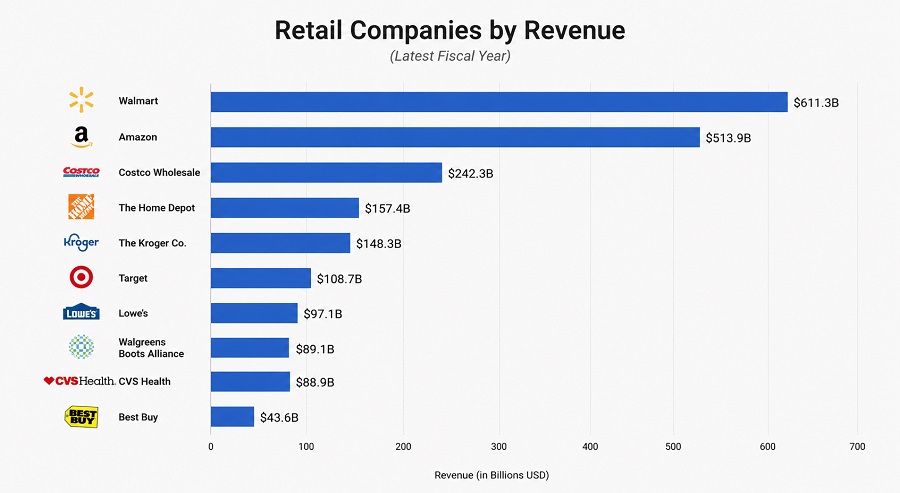

Chart: revenue gap inside the Top 10

The Top 10 is not evenly spaced. Walmart sits in a separate scale tier; Amazon and Costco are close to each other; Schwarz Group, Home Depot and Kroger form the next revenue band. The chart is useful for seeing those breaks, not just the rank order.

Top 10 retail revenue, shown in US$ billions for readability.

Top 100 retail companies by revenue

Share view uses Deloitte’s Top 250 aggregate retail revenue of US$6.03 trillion. It shows each company’s share of the Top 250 total, not its share of all global retail spending.

| Rank | Company | Country | Retail revenue |

|---|---|---|---|

| 1 | Walmart | United States | $648,125M10.75% |

| 2 | Amazon | United States | $251,902M4.18% |

| 3 | Costco | United States | $242,290M4.02% |

| 4 | Schwarz Group | Germany | $177,009M2.94% |

| 5 | The Home Depot | United States | $152,669M2.53% |

| 6 | The Kroger Company | United States | $148,905M2.47% |

| 7 | Aldi | Germany | $123,608M2.05% |

| 8 | JD.com | China | $122,884M2.04% |

| 9 | Walgreens Boots Alliance | United States | $121,191M2.01% |

| 10 | CVS Health | United States | $116,763M1.94% |

| 11 | Target Corporation | United States | $105,803M1.75% |

| 12 | Ahold Delhaize | Netherlands | $97,837M1.62% |

| 13 | Carrefour | France | $90,803M1.51% |

| 14 | Lowe's | United States | $86,250M1.43% |

| 15 | Tesco | United Kingdom | $85,218M1.41% |

| 16 | Albertsons | United States | $79,238M1.31% |

| 17 | Edeka | Germany | $75,930M1.26% |

| 18 | LVMH | France | $73,299M1.22% |

| 19 | Seven & I Holdings | Japan | $72,750M1.21% |

| 20 | E.Leclerc | France | $63,229M1.05% |

| 21 | Rewe Group | Germany | $62,735M1.04% |

| 22 | Aeon | Japan | $58,671M0.97% |

| 23 | Publix | United States | $57,100M0.95% |

| 24 | TJX Companies | United States | $54,217M0.90% |

| 25 | Loblaw Companies | Canada | $44,012M0.73% |

| 26 | HE Butt Grocery | United States | $43,600M0.72% |

| 27 | Best Buy | United States | $43,452M0.72% |

| 28 | Les Mousquetaires | France | $43,377M0.72% |

| 29 | IKEA | Netherlands | $42,960M0.71% |

| 30 | Woolworths Group | Australia | $42,005M0.70% |

| 31 | Sainsbury's | United Kingdom | $40,580M0.67% |

| 32 | Inditex | Spain | $38,935M0.65% |

| 33 | Dollar General | United States | $38,692M0.64% |

| 34 | Coop | Switzerland | $36,794M0.61% |

| 35 | Mercadona | Spain | $36,267M0.60% |

| 36 | Auchan | France | $35,590M0.59% |

| 37 | Jeronimo Martins | Portugal | $33,780M0.56% |

| 38 | Asda | United Kingdom | $32,611M0.54% |

| 39 | Groupe ADEO | France | $31,952M0.53% |

| 40 | Reliance Retail | India | $31,002M0.51% |

| 41 | Migros | Switzerland | $30,688M0.51% |

| 42 | Shein | Singapore | $30,666M0.51% |

| 43 | Dollar Tree | United States | $30,604M0.51% |

| 44 | Cooperative U | France | $30,360M0.50% |

| 45 | Coles Group | Australia | $29,061M0.48% |

| 46 | FEMSA | Mexico | $26,839M0.45% |

| 47 | CP All | Thailand | $25,998M0.43% |

| 48 | EssilorLuxottica | France | $25,964M0.43% |

| 49 | Alibaba Group New Retail & Direct Sales | Hong Kong | $24,890M0.41% |

| 50 | Metro AG | Germany | $24,679M0.41% |

| 51 | Ceconomy | Germany | $23,516M0.39% |

| 52 | AS Watson Group | Hong Kong | $23,479M0.39% |

| 53 | Macy's | United States | $23,092M0.38% |

| 54 | H&M | Sweden | $22,621M0.38% |

| 55 | Empire Company | Canada | $22,400M0.37% |

| 56 | Nike Direct | United States | $22,351M0.37% |

| 57 | Wesfarmers | Australia | $22,288M0.37% |

| 58 | Meijer | United States | $21,950M0.36% |

| 59 | Coupang | South Korea | $21,223M0.35% |

| 60 | Ross Stores | United States | $20,377M0.34% |

| 61 | BJ's Wholesale Club | United States | $19,969M0.33% |

| 62 | Conad | Italy | $19,866M0.33% |

| 63 | Berkshire-Hathaway Retail | United States | $19,408M0.32% |

| 64 | Fast Retailing | Japan | $18,964M0.31% |

| 65 | Wm Morrison Supermarkets | United Kingdom | $18,776M0.31% |

| 66 | Alimentation Couche-Tard | Canada | $17,536M0.29% |

| 67 | AutoZone | United States | $17,457M0.29% |

| 68 | Kering | France | $17,047M0.28% |

| 69 | e-mart | South Korea | $17,017M0.28% |

| 70 | Cencosud | Chile | $16,768M0.28% |

| 71 | Richemont | Switzerland | $16,662M0.28% |

| 72 | Kohl's | United States | $16,586M0.28% |

| 73 | Marks & Spencer | United Kingdom | $16,541M0.27% |

| 74 | Kingfisher | United Kingdom | $16,472M0.27% |

| 75 | Coop Italia | Italy | $16,334M0.27% |

| 76 | Spar Holding | Switzerland | $16,330M0.27% |

| 77 | O'Reilly Automotive | United States | $15,812M0.26% |

| 78 | S Group | Finland | $15,681M0.26% |

| 79 | Chedraui | Mexico | $15,407M0.26% |

| 80 | Dirk Rossmann | Germany | $15,341M0.25% |

| 81 | Metro Inc. | Canada | $15,259M0.25% |

| 82 | Avolta | Switzerland | $14,949M0.25% |

| 83 | Gap | United States | $14,889M0.25% |

| 84 | Vipshop | China | $14,875M0.25% |

| 85 | Otto | Germany | $14,657M0.24% |

| 86 | Tractor Supply Company | United States | $14,556M0.24% |

| 87 | Genuine Parts Company | United States | $14,247M0.24% |

| 88 | Nordstrom | United States | $14,219M0.24% |

| 89 | ICA Gruppen | Sweden | $14,188M0.24% |

| 90 | Chow Tai Fook | Hong Kong | $13,891M0.23% |

| 91 | Assai Atacadista | Brazil | $13,701M0.23% |

| 92 | John Lewis Partnership | United Kingdom | $13,684M0.23% |

| 93 | Hermes | France | $13,485M0.22% |

| 94 | El Corte Ingles | Spain | $13,372M0.22% |

| 95 | Menards | United States | $13,240M0.22% |

| 96 | Shoprite Holdings | South Africa | $13,225M0.22% |

| 97 | JD Sports | United Kingdom | $13,080M0.22% |

| 98 | Hy-Vee | United States | $13,000M0.22% |

| 99 | Decathlon Group | France | $12,993M0.22% |

| 100 | Dick's Sporting Goods | United States | $12,984M0.22% |

Coverage: 100 companies. Source basis: Deloitte Global Powers of Retailing 2025, FY2023 retail revenue, US$ millions.

Methodology

The indicator is retail revenue, measured in US dollars. Retail revenue can differ from total corporate revenue when a group has large non-retail activities. The ranking follows Deloitte Global Powers of Retailing 2025, which covers FY2023 financial years ending from 1 July 2023 to 30 June 2024.

The values are FY2023 retail revenues from Deloitte’s 2025 edition. They are rounded to the nearest US$ million in the source table. Share values are calculated against the Top 250 aggregate retail revenue of US$6.03 trillion reported in the same edition, so they describe concentration inside Deloitte’s Top 250 universe rather than the entire global retail market.

Comparability limits remain important. Fiscal calendars differ, exchange-rate conversion affects non-US companies, and private retailers may rely on reported or estimated figures. Retail groups also vary by format: grocery, pharmacy, e-commerce, luxury, home improvement and discount retail have different margins, capital needs, inventory cycles and labour intensity.

Insights from the ranking

- Scale defines the top of the ranking: Walmart’s retail revenue is more than twice Amazon’s retail revenue in this dataset.

- Food retail and pharmacy remain structurally large because they capture recurring household spending and high purchase frequency.

- European strength is concentrated in discounters, supermarket cooperatives and cross-border grocery groups rather than general merchandise giants.

- E-commerce scale is visible through Amazon, JD.com, Shein, Coupang, Vipshop and Otto, but store networks still dominate many positions because grocery, pharmacy and discount formats generate very high transaction frequency.

- The lower half of the Top 100 is more format-diverse, with apparel, auto parts, luxury, travel retail, sporting goods and department stores. These companies can be smaller by revenue while still having stronger margins or brand economics than some mass retailers.

What the ranking means for readers

For consumers, the ranking helps explain why the same retailers influence prices, delivery expectations, product availability and private-label competition across many markets. The largest retailers can invest heavily in logistics, data systems, advertising platforms and supplier negotiations.

For investors and analysts, revenue scale should not be confused with profitability. Grocery and warehouse clubs can be huge but low-margin, while luxury and specialty retail can be smaller but more profitable. For policy readers, the table shows where supplier bargaining power, labour scale, data advantages and cross-border retail influence are concentrated.

FAQ

Is this actual 2026 revenue?

No. The company figures are FY2023 retail revenues from Deloitte’s 2025 edition. The 2026 wording reflects the page update cycle, not a new financial year for the companies.

Why is Amazon not ranked first here?

This table uses retail revenue from the source methodology, not total consolidated company revenue. Amazon has major non-retail revenue streams, especially cloud services, so its retail-revenue position differs from its total corporate scale.

Why are some private companies included?

The Deloitte ranking includes public and private retailers where comparable revenue data are available or estimated through the source methodology.

Why use retail revenue instead of market capitalization?

Revenue measures operating scale. Market capitalization measures investor valuation and includes expectations about margins, growth and risk.

Can different fiscal years affect the ranking?

Yes. The source standardizes inclusion by fiscal years ending within a defined 12-month window, but companies still report under different fiscal calendars and currencies. That matters most when exchange rates or inflation move sharply.

Sources

- Deloitte — Global Powers of Retailing 2025: primary source for retailer performance, FY2023 coverage, aggregate retail revenue and methodology context.

- NRF and Kantar — Top 50 Global Retailers 2025: supporting cross-check for retailer scale and international footprint.

- Deloitte — Global Retail Outlook: sector context on technology, cost pressure and operating change.

Last updated: May 2026. Company figures are FY2023 retail revenues from Deloitte Global Powers of Retailing 2025.

Related rankings

More StatRanker rankings on public finance, tax burden, debt and government spending.

Top 100 Defense Companies by Revenue, 2026 Snapshot

Open rankingTop 100 Pharma Companies by Revenue in 2026

Open rankingTop 30 Companies by Revenue, 2026

Open rankingTop 1000 Global Companies by Revenue (Sales), Latest FY

Open rankingStatRanker (Website)

administrator